Aggressive EA Strategy: Why Our Core+Per-Pair Crumbled Under Costs

## What's the idea?

A beginner-friendly summary of the verification: “Aggressive EA Strategy: Why Our Core+Per-Pair Crumbled Under Costs”.

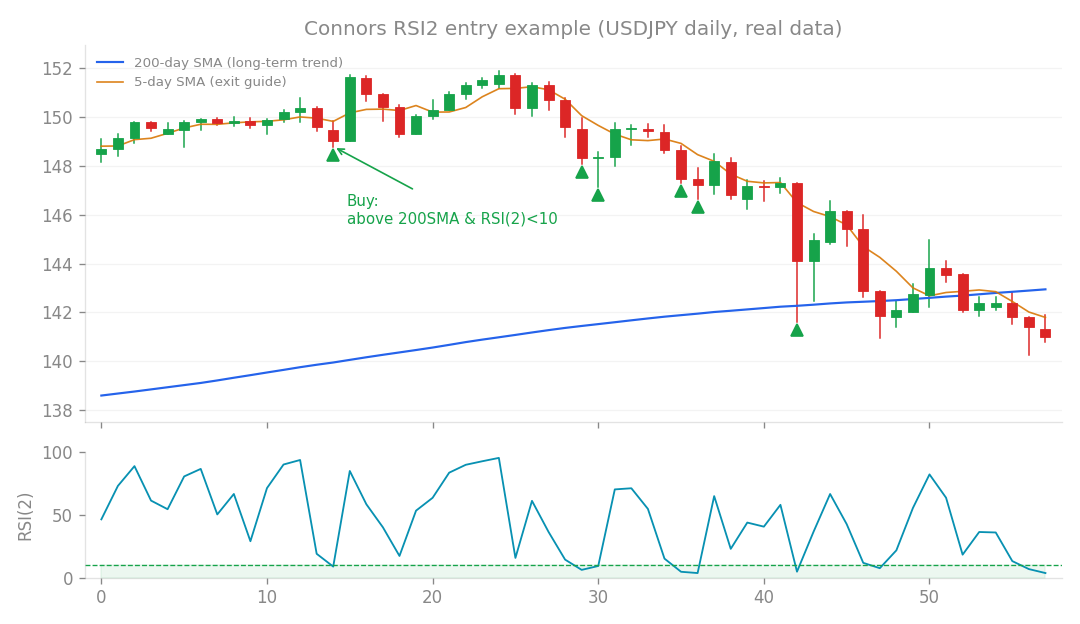

Connors RSI2 entry example (USDJPY daily, real data): buy the dip when price is above the 200-day SMA and RSI(2) falls below 10.

What’s the idea?

We all dream of EAs that can churn out consistent profits, but what happens when those strategies meet the real-world costs of live trading? That’s exactly what we wanted to investigate. We put two types of strategies under the microscope: a more conservative “Core” approach and an “Aggressive Per-Pair” setup. Our main question was: how do these perform once we factor in actual trading costs like spreads and commissions? We specifically suspected that the aggressive strategy, with its shorter trade durations, might be much more sensitive to these costs.

How I tested it

To test this, we simulated live trading conditions for our “Aggressive Per-Pair” strategy. This strategy is designed to manage individual currency pairs, often with shorter holding periods. For instance, some components using Donchian or ATR indicators held trades for a mere 1.2 to 1.3 days. A particularly fast component, “FX Connors” (likely a specific tactical system), had an incredibly short average holding period of just 0.2 days—that’s less than 5 hours per trade! In contrast, our “Core” strategy typically holds trades for a much longer average of 6.8 days. We then added a realistic cost burden to every single trade: an extra 1 pip of spread/slippage plus a $7 commission per standard lot traded. To give you an idea of the volume, the FX Connors component alone generated about 1550 trades during the testing period. More trades mean more opportunities for these costs to add up!

What happened?

The results were quite eye-opening, especially for the aggressive strategy. The Aggressive Per-Pair Strategy:

- Under the “Current Regime” (favorable market conditions): Even in what should have been a good environment, the monthly return for the aggressive strategy dropped significantly from 2.43% to 1.86% after accounting for costs. That’s a 23% reduction in profit! While still attractive, it’s a noticeable hit. The maximum drawdown (DD), which is the largest peak-to-trough decline in capital, was 10.4%.

- Over the Full Testing Period: When we looked at the strategy’s performance across a broader range of market conditions (the “full period”), the impact of costs was even more severe.

- Monthly returns plummeted from 1.38% down to just 0.91%.

- The maximum drawdown (DD) more than doubled, worsening from an already concerning -14% to a hefty -28%!

- Our “capital retention rate” (MC), a measure of how much capital remained or the strategy’s overall resilience, dropped sharply from 89% to a mere 69%. In other words, the strategy became significantly more fragile and risked losing more of the initial capital.

- This clearly showed that the aggressive strategy was quite brittle when faced with both real trading costs and less favorable market conditions (a “weak regime”). The Impact of FX Connors: We also investigated the role of the super-fast “FX Connors” component. When we removed it from the aggressive strategy for the full period, things improved slightly: the drawdown was -25% (better than -28%), and the capital retention rate was 74% (better than 69%). This suggested that for live trading, it might be wise to exclude such extremely short-term, high-frequency components to mitigate cost impact. The Conservative Core Strategy (A Stark Contrast): In stark contrast, our “Core” strategy proved to be incredibly robust against these real-world costs. Its Profit Factor (PF = gross profit / gross loss; anything >1 means profitable) remained excellent at 5.77, indicating strong profitability relative to losses. It even benefited from positive swap rates, which can sometimes provide a small tailwind. Its monthly return only saw a modest reduction of about 7% due to costs. This strategy was, in a word, “cost-super-resilient.”

What I learned

The main takeaway is crystal clear: aggressive strategies, especially those with very short holding periods, are significantly more vulnerable to real trading costs than more conservative, longer-term approaches. It’s like death by a thousand paper cuts—each small cost adds up rapidly when you’re trading frequently. Here’s what this means for your EA trading:

- Understand the Fragility of Aggressive Strategies: If you’re running an aggressive, high-frequency EA, you must understand its inherent weakness against real trading costs.

- Conservative Risk Management is Key: For aggressive EAs, it’s essential to be extremely conservative with your risk settings. We’re talking about reducing risk parameters significantly (e.g., to around 0.002). This means trading smaller sizes relative to your capital.

- Aggressive EAs are for “Upper-Bound Aiming” (in Favorable Regimes): Don’t expect aggressive strategies to be consistent, long-term earners. They are best suited for trying to capture larger upward swings during specific, favorable market conditions (like the “current regime” we observed). They are not built for steady, reliable withdrawals.

- For Steady, Consistent Withdrawals, Choose Conservative: If your goal is reliable, consistent withdrawals from your trading account, our “Core” (conservative, standalone) strategy is strongly recommended. Its robustness to costs makes it a far more dependable choice for long-term growth.

- Know Your Tool’s Purpose: Ultimately, it comes down to using the right tool for the right job. Conservative strategies are your sturdy workhorses, built to withstand the bumps and costs of real trading. Aggressive strategies are more like sports cars—exciting, potentially high-reward in ideal conditions, but much more sensitive and prone to breaking down under pressure.