Monthly 3% in FX EA: Dream or Reality? Unveiling the True Cost & Limits!

## What's the idea?

A beginner-friendly summary of the verification: “Monthly 3% in FX EA: Dream or Reality? Unveiling the True Cost & Limits!”.

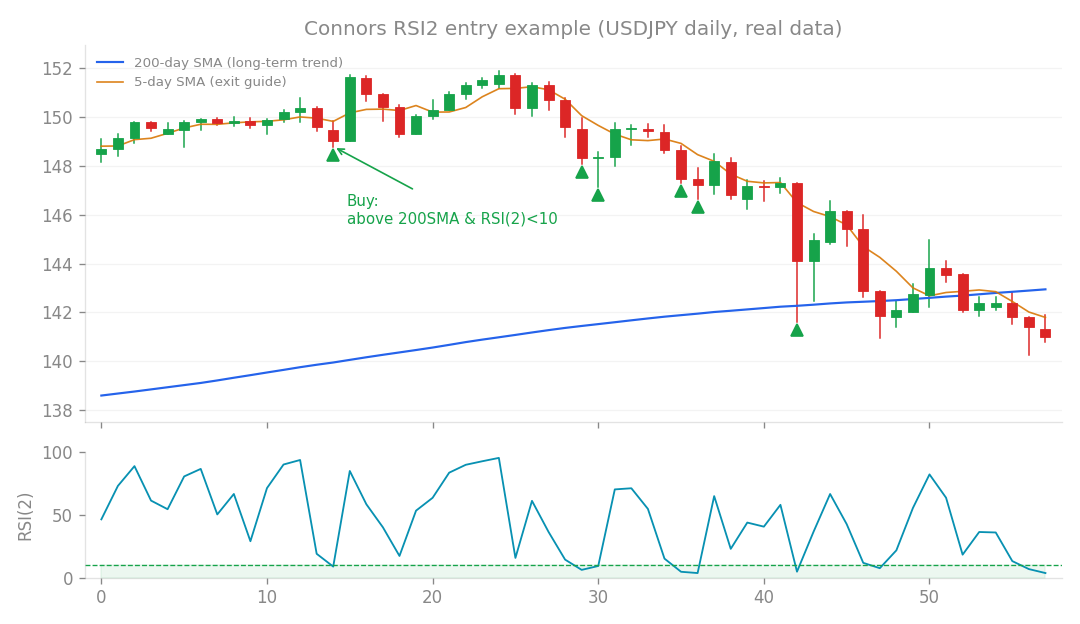

Connors RSI2 entry example (USDJPY daily, real data): buy the dip when price is above the 200-day SMA and RSI(2) falls below 10.

What’s the idea?

Many of you dream of hitting a consistent 3% return every month from your FX EAs. It’s a tempting number, promising significant growth. But is that a realistic, sustainable goal, or just a pipe dream? That’s exactly what we set out to quantify in this research. Our aim was to see how much we could push the “aggressiveness” of a combined EA strategy and what impact that had on key performance metrics. We took a blend of proven approaches – a “core” system, alongside six different indicators, and even incorporated a Connors-style strategy. The big question: could we bundle these together, crank up the risk, and safely hit that 3% monthly target?

How I tested it

To figure this out, we systematically ramped up the “aggressiveness multiplier” of our combined EA. Think of it like turning up the volume knob on your trading – more aggressive means bigger position sizes relative to your capital. For each level of aggressiveness, we measured four crucial metrics to get a full picture of performance and risk:

- Monthly Return: This is straightforward – the average profit percentage your account gained each month.

- Drawdown (DD): Super important! This is the peak-to-trough decline in your account balance during a specific period. Imagine your account hits a high point, then drops before recovering; the DD is that percentage drop. A smaller DD means less risk and stress on your capital.

- Max Drawdown (MC): This is the single largest percentage drop your account experienced from its highest point to its lowest point before making a new high. It’s the worst-case scenario you might face.

- Calmar Ratio: This is a fantastic metric for comparing risk-adjusted returns. It’s calculated as (Annualized Return / Max Drawdown). In other words, it tells you how much return you’re getting for each unit of risk you’re taking. A higher Calmar Ratio is better, indicating more efficient returns!

What happened?

The results were a real eye-opener, and honestly, a bit sobering. First off, we saw a clear, almost linear relationship between our monthly return target and the drawdown we experienced. It’s like a seesaw: the higher you want your monthly profit to go, the deeper your potential drawdowns get. Crucially, the Calmar Ratio, which tells us about risk-adjusted returns, seemed to hit a ceiling. Even after optimizing allocations, adding those six indicators, and throwing in the Connors strategy, the Calmar Ratio consistently topped out at around 1.0 to 1.3. What does that mean? It means that beyond a certain point, increasing your returns just brings proportionally more risk, not more efficient returns. You’re not getting “smarter” profits; you’re just taking bigger bets. Let’s look at the numbers:

- If we wanted to keep our Drawdown to 10% or less (a pretty sensible safety limit for many traders), the maximum monthly return we could realistically achieve was only about 0.6%. In other words, to keep your account relatively safe, you’re looking at modest, consistent gains.

- Pushing for higher returns quickly escalated the risk:

- Aim for 1.1% monthly return? You’re looking at a 24% Drawdown.

- Want 2.0% monthly return? Prepare for a hefty 49% Drawdown.

- Reaching for 2.65% monthly return? That came with a staggering 69% Drawdown.

- And for our original target of 3% monthly return? Our models predicted a Drawdown of around -70%. In plain English: that’s pretty much an account wipeout!

What I learned

The big takeaway is stark but important: Achieving a consistent 3% monthly return with a “safe” drawdown (meaning, keeping your account alive and well) is mathematically impossible with these types of strategies and market conditions. Let me explain why. To hit an annual return of 36% (which is 3% monthly) with a maximum drawdown of, say, 10% (a generally accepted level for “safe” capital preservation), you would need a Calmar Ratio of 3.6 (36% / 10%). Think about that for a second. A Calmar Ratio of 3.6 is the kind of performance you’d see from only the absolute elite hedge funds in the world, often employing extremely sophisticated strategies across multiple markets and with vast resources. Our real-world tests, using trend-following edges from price and indicators, consistently showed a Calmar Ratio in the 1.0 to 1.3 range. This is a perfectly respectable Calmar for many automated strategies, indicating a decent return for the risk taken, but it’s nowhere near the 3.6 needed for that “safe” 3% monthly. Yes, you could technically achieve 3% monthly by cranking up the leverage to insane levels. But as our data showed, that comes with a ~70% drawdown. That’s not a “3% monthly income”; it’s a nearly guaranteed path to bankruptcy. We refuse to build or promote systems based on such unrealistic promises.

So, what now? Realistic Paths Forward

So, if the dream of 3% monthly with safety is out the window, what can you do? It’s important to be realistic and adapt your approach. Here are some actionable paths forward:

- Adjust Your Expectations and Scale Up: The data suggests that a more achievable and sustainable monthly target with reasonable drawdown (e.g., keeping DD below 10%) is closer to 0.6% per month. If you need more income from your trading, the answer isn’t necessarily higher risk with the same strategy; it’s scaling up your capital. This means either increasing your account size or diversifying across multiple accounts running the same safe strategy.

- Explore New Frontiers: The Calmar Ratio is dependent on the inherent “edge” available in a particular market or asset class. It’s possible that other asset classes, like cryptocurrencies, might offer different underlying dynamics that could lead to a better Calmar Ratio. This would require fresh, rigorous research and testing, of course!

- Accept the Gamble (If You Must): If a 3% monthly return is an absolute must-have for you, you have to accept that it’s not an “investment” but a “one-shot gamble.” You’re essentially betting your entire account on a very high-risk, high-reward scenario, understanding that the probability of significant loss (or total wipeout) is extremely high. This is not a strategy we recommend for building sustainable wealth, but it’s important to be honest about what you’re getting into.